Should I Settle My Balance Before Applying?

Settling first can improve your odds — but timing matters. When a settlement helps, when to skip it, and what a settlement letter unlocks.

Whether to settle a broken-lease balance before you apply is one of the most consequential decisions in the placement process. Do it in the right circumstances and your options widen and your risk fees drop. Do it in the wrong circumstances and you waste weeks negotiating for no benefit — or worse, re-age a collections account. This guide walks through when to settle first, when to skip it, and how urgency changes the calculation.

When settling helps

Settling helps when:

- The balance is a hard denial trigger at your target communities. Some communities’ automated screens configure any unpaid rental balance over a threshold amount as an auto-decline. A settlement resolves the trigger.

- You’re planning multiple applications. A settlement letter you can attach to every application streamlines the process across the shortlist instead of relitigating unpaid status at each community.

- You want a no-risk-fee approval. Some communities skip the risk fee entirely for paid or settled broken leases. If your target list includes communities like that, settling pays for itself.

- You have time. Settlements often take 2-4 weeks to negotiate, execute, and get documentation for. If your move-in date is 6+ weeks out, that’s a fine timeline.

When settling doesn’t help (or hurts)

Settling doesn’t help when:

- Your target communities are case-by-case reviewers who don’t distinguish paid from unpaid. Some communities treat any recorded broken lease the same way. Settling doesn’t change the outcome, and you’ve spent the money for nothing.

- You need to move now. If your target move-in date is 2 weeks out, the settlement negotiation won’t finish in time. Applying to friendly communities immediately is often the right move.

- The debt is old and in collections. Paying an old collection can, with some scoring models, reset the “date of last activity” on the account — making it look newer on your credit report. If you’re renting and not applying for a mortgage next month, this rarely matters for approval — but it’s worth knowing.

The negotiation itself

If you decide to settle, the process:

- Request debt validation in writing from whoever holds the balance (former community or collection agency). This confirms the debt is yours and the amount is accurate.

- Negotiate a reduced payoff. Common outcome: 40-70% of the original balance, though every situation is different.

- Get the settlement terms in writing before paying. The written agreement should state the reduced amount, that payment resolves the balance in full, and (ideally) that the account will be reported as paid/settled going forward.

- Pay via traceable method (bank check, wire, or trackable payment) and keep the receipt.

- Request the settlement/paid letter as a condition of payment. Some agencies will send it automatically; others need to be asked explicitly.

The letter is the artifact that matters for your rental application. Without it, the settlement is invisible.

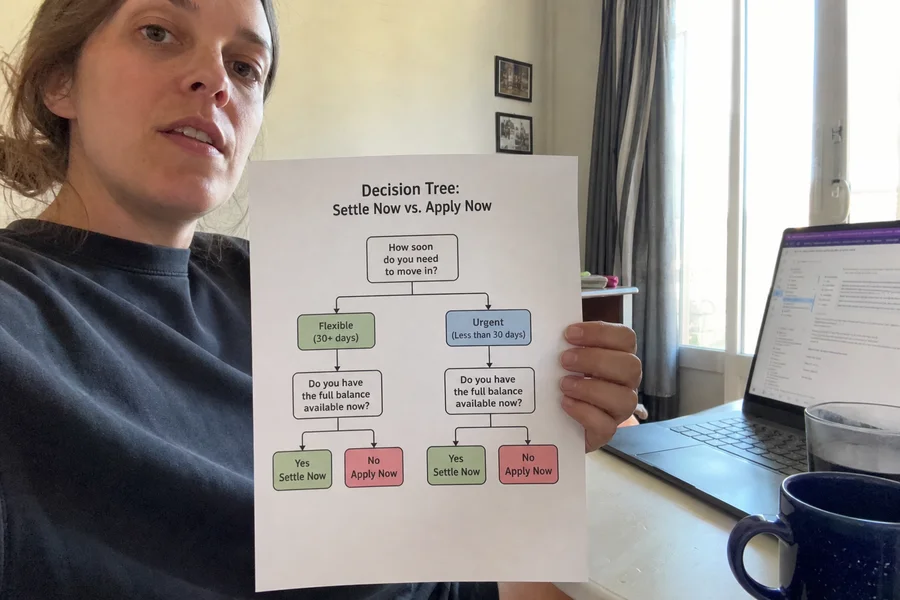

The urgency-vs-settlement trade-off

Our agents run this decision with you before you commit either way. A rough decision framework:

- Move-in date > 6 weeks out, balance > $1,000, target communities that distinguish paid from unpaid: Settle first.

- Move-in date < 4 weeks out: Apply first. Consider settling in parallel if you can, but don’t wait.

- Balance < $500 and you can pay in full: Pay it. Fast and simple.

- Balance in collections at an old agency with a strong statute defense: Consider the Texas 4-year statute route before deciding to pay at all.

Related reading

Frequently asked

Does settling guarantee approval?

No. Settling removes a common denial trigger and widens your options, but it doesn't override a community's other criteria (income, timing, other rental-history issues).

Is settling the same as paying in full?

No. Settling is a reduced payoff — you and the community/agency agree on less than the full balance. Some communities treat settled and paid the same; others don't. The settlement letter's wording matters.

Should I settle if I need to move fast?

Sometimes applying first is smarter. If a case-by-case community will approve without settlement, delaying to negotiate can cost you the timeline. Our agents weigh timing with you.

Turn this into a placement.

Our agents will match you with Texas communities that fit your specific scenario.