Two separate checks, two separate flags

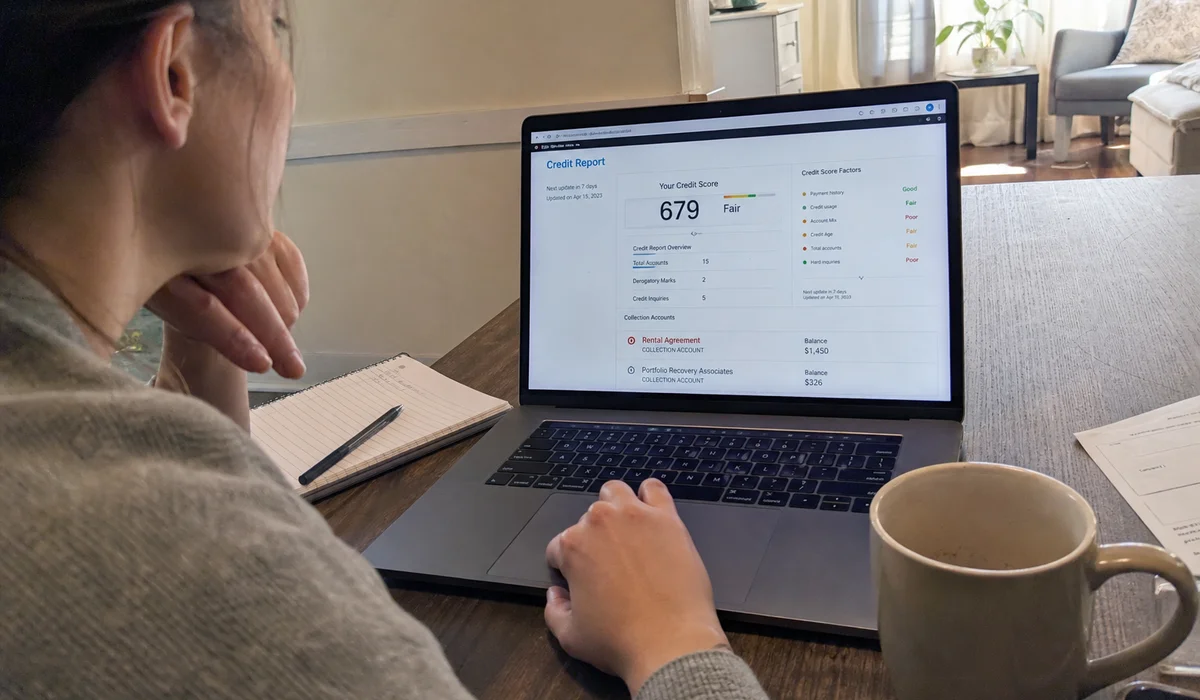

A broken lease in collections is a double hit. First, it appears on your rental-history screening report — showing the former community, the balance owed, and the date. Second, it appears on your credit report as a collections account, tied to the agency that took over the debt. Two separate systems. Two chances for a community to see it and stop reading.

That’s the surface problem. The deeper problem is that a lot of PMCs weight rental collections harder than other collections. A medical collection or a card collection from the same era barely registers with some communities; a rental collection registers as “this person didn’t pay their last landlord.”

Some communities. Not all. That’s the opening.

The agencies actually holding your debt

Most Texas multifamily rental debt ends up with National Credit Systems or IQ Data International. These agencies buy or collect on rental balances from apartment communities and then report the accounts to the credit bureaus.

Both negotiate. Both will accept less than the full balance in many cases. Both will provide a paid-in-full or settled letter if you request it as a condition of payment. The key steps: request debt validation first (it confirms the debt is yours and accurate), negotiate the reduced payoff, and get the settlement terms in writing before you send any money.

The pay-vs-settle-vs-wait decision

Paying a collection in full is the strongest signal for housing screening, but there’s a catch: with some scoring models, paying a very old collection can update the “date of last activity” and make the account look newer on your credit report. If you’re renting and not applying for a mortgage next week, this rarely matters for approval — but it’s worth knowing.

Settling for less is often the practical middle path. You resolve the balance for something you can afford, get the paperwork you need, and don’t accidentally re-age anything if your negotiation includes a no-re-age term.

Waiting is a real option too. Texas has a 4-year statute of limitations on written contracts, including leases. After 4 years, the debt can’t be sued for. It still appears on your reports, but the negotiation leverage flips — collection agencies often accept lower settlements on debt past the statute because they can no longer legally pursue it.

Here’s how the three paths compare at a glance:

| Path | Best When | Main Trade-Off |

|---|---|---|

| Pay in Full | You can afford it and want the strongest signal | May re-age an old account on credit |

| Settle for Less | You want resolution you can afford | Wording must confirm the balance is resolved |

| Wait (past 4-yr statute) | Debt is old and not affordable now | Still appears on reports until it ages off |

Communities that read collections lightly

Some Texas PMCs have policies that read: “Collections older than 24 months not considered.” Some read: “Rental collections weighted the same as other collections.” Some read: “Any collection over $500 is a decline.” Which policy your target community follows changes everything.

Our list to you names communities that either don’t weight rental collections heavily or approve when the collection is documented as paid, settled, or past the statute. That’s the working shortlist — the same case-by-case approach we use to find apartments that accept broken leases across every Texas metro we cover.