Does Paying a Collection Reset the Reporting Clock?

With some scoring models, paying can re-date a collection and make it look newer. When paying hurts, when it helps, and safer alternatives.

As a professional service team, we hear the same frustrating question from business owners and homeowners every week regarding old accounts. Paying off a debt seems responsible, yet many wonder: does paying collection reset clock limits on a credit report?

The truth is that the outcome depends entirely on the scoring model, the reporting agency, and your specific financial goals. Our team understands how stressful this uncertainty can be for your financial plans.

Let’s break down how this process works and review concrete strategies to avoid a bad outcome.

The re-aging concept

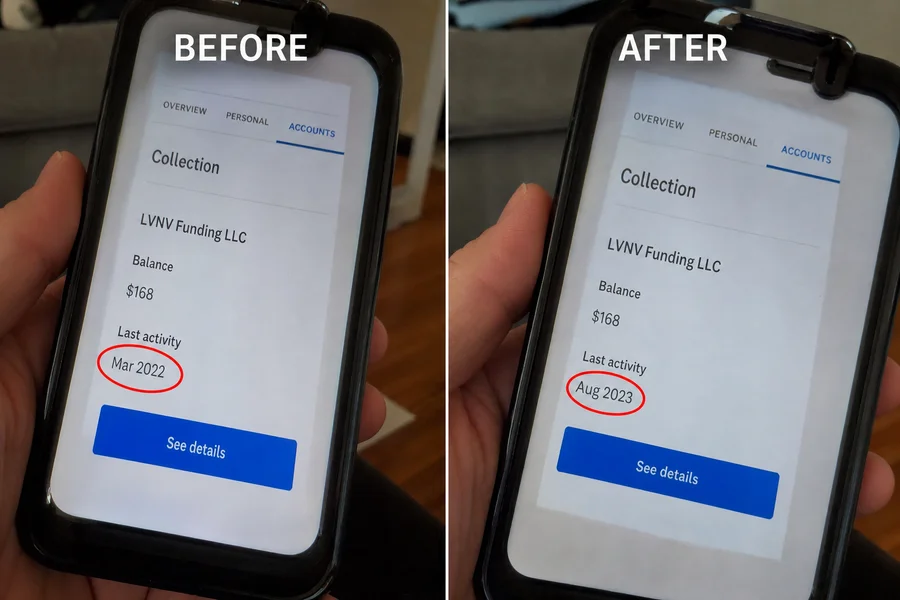

Paying a collection does not legally reset credit reporting clock limitations, but it can update the date of last activity on your file. We refer to this technical penalty as a situation where paying collection re-ages account profiles. This update can cause older scoring models to penalize you for recent negative activity, effectively lowering your score.

The Fair Credit Reporting Act (FCRA) mandates that negative items fall off seven years from the original date of delinquency. Our experts always advise clients that a payment update simply changes the Date of Last Activity (DLA). That clock starts roughly 180 days after your first missed payment, not the date the debt went to collections.

Scoring algorithms read a recent DLA and assume the financial distress is fresh. An account with a DLA from three years ago scores differently from an account updated three months ago, even if the underlying debt is identical. We track several major exceptions to this general rule across the US market.

- Medical debts under $500 and all paid medical collections are no longer reported.

- Our data shows that FICO 8 ignores collections with original balances under $100.

- Newer models do not penalize you for doing the right thing.

Which scoring models re-age

The impact of a paid collection depends entirely on which credit bureau algorithm reviews your file. We see a highly fragmented landscape across the US financial sector today. Newer systems ignore paid collections, while older systems used by traditional banks still penalize them.

Different lenders pull very different scores depending on the loan type.

The Modern Consumer Models

Our favorite modern algorithms, like FICO 9 and VantageScore 4.0, dominate credit card and personal loan decisions. These systems completely ignore paid collection accounts. Settling an old debt is a clear win if your lender uses these models.

The Transitional Mortgage Models

We consider the upcoming mortgage underwriting changes in 2026 to be a huge advantage for modern homebuyers. The Federal Housing Finance Agency (FHFA) now allows lenders to use VantageScore 4.0 alongside older models. Older systems like FICO 2, FICO 4, and FICO 5 still treat paid and unpaid collections similarly.

We warn applicants that a recent payment on an old debt could trigger a DLA update and lower these specific classic scores.

Specialized Housing Systems

Property managers use proprietary screening tools like Experian RentBureau or SafeRent. These specific rental models view paid collections favorably.

Our records show that clearing an old balance will almost always improve your odds of securing a lease. Paying rarely hurts when you are strictly looking for an apartment approval.

How to avoid re-aging

You can prevent a score drop by negotiating a written agreement before sending any money. We always advise securing these exact terms in a physical document first. Disputing improper updates with the bureaus is your fallback plan if an agency breaks their promise.

Two specific levers give you control over the reporting process.

Request a Pay-For-Delete Agreement

Our standard approach is asking the collection agency to completely remove the tradeline upon payment. Collection agencies frequently buy debt for pennies on the dollar. You can often start a settlement offer at 25 to 30 percent of the original balance.

We know that getting this specific commitment in writing guarantees the negative mark vanishes from Equifax, Experian, and TransUnion.

Secure a No Re-Age Clause

If an agency refuses a complete deletion, request a written commitment that they will not update the DLA field. Reputable firms like NCS or IQ Data will often honor this request if negotiated upfront.

We warn clients that paying without this clause leaves them vulnerable to an automatic system update. You must get the no-update promise signed before handing over your credit card.

Dispute Improper Bureau Updates

Sometimes a collector updates the activity date despite signing a written agreement. Our partners in the mortgage industry often recommend requesting a rapid rescore in these situations. You can file a formal dispute with the credit bureaus using your settlement letter as hard proof.

This specialized process forces a bureau update in three to five business days instead of the standard month.

When paying still makes sense (despite the risk)

We recommend settling an account if you fit into specific renter or timeline categories. Settling a collection is generally the right move for those aiming for long-term financial health. The minor risk of a temporary score drop is usually outweighed by the benefits of clearing the debt.

- Our property management contacts treat paid collections as resolved accounts during the rental application process.

- Systems like FICO 9 and VantageScore 4.0 do not penalize you at all.

- Making a payment stops aggressive legal action if the debt is still within your state’s statute of limitations.

- We remind clients that once past the seven-year FCRA window, the account falls off entirely regardless of the DLA.

The re-aging concern is most relevant if you plan to use your credit for a large decision in the near term. Applying for a mortgage or a major auto loan requires careful timing.

We strongly suggest talking to a mortgage broker before paying an old collection if you plan to buy a house this year. If you still find yourself asking, “does paying collection reset clock deadlines for my report,” review your personal credit file today. Map out a clear plan before sending a check.

Related reading

Frequently asked

Does paying always re-age a collection?

No. Whether it re-ages depends on the scoring model and how the agency reports the update. FICO 8 and 9, for example, don't treat paid collections the same as unpaid, but some older models do.

How do I avoid re-aging?

Negotiate settlement terms that explicitly don't update the date of last activity, and get that in writing. Reputable agencies will honor this.

Is it ever safe to just pay?

For housing screening purposes, usually yes — paid collections read favorably regardless of the date. The concern is credit-score-driven decisions like mortgage applications.

Turn this into a placement.

Our agents will match you with Texas communities that fit your specific scenario.