The pitch, and the catch no one tells you

A third-party guarantor company co-signs your lease for a fee — typically 5%-12% of annual rent, on top of your deposit and first month. On the community’s side, the guarantor covers the financial risk of the lease. On your side, you get a shot at communities that otherwise wouldn’t approve you.

The catch: guarantors solve financial risk, not behavioral risk. Some communities won’t accept a guarantor for a broken lease because they view the break itself as a pattern concern, not just a money problem. Those communities will happily take a guarantor from a renter with thin credit or short employment — but not from a renter with a broken lease on record.

Which communities fall on which side of that line is the thing our agents track.

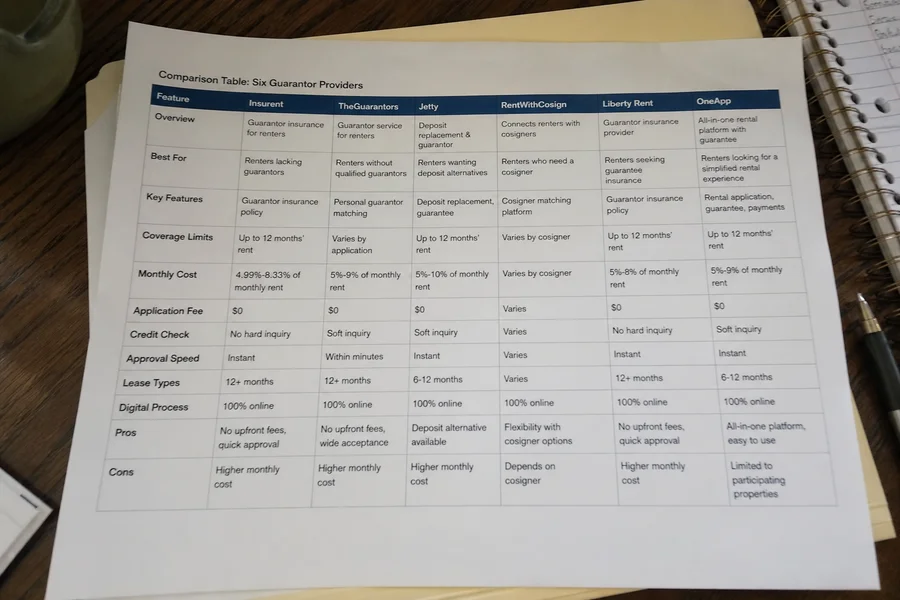

The six providers you’ll actually see in Texas

Insurent is one of the oldest and most widely accepted. Fee typically 6%-13% of annual rent. Underwriting around 27.5x monthly rent in income.

TheGuarantors offers different tiers with fees usually 5%-10% of annual rent. Slightly more flexible underwriting; sometimes uses employment history and credit together.

Jetty covers guarantor plus renter-friendly financial products. Fee typically 5%-10%. Popular at newer, larger PMC portfolios.

RentWithCosign targets renters who wouldn’t qualify at the majors. Higher fee, more flexible underwriting. Not accepted everywhere.

Liberty Rent offers guarantor plus lease-insurance products. Underwriting varies by community relationship.

OneApp Guarantee is a newer entrant with more flexible income thresholds and a growing acceptance list.

Every provider has its own underwriting, so the same renter may qualify at one and not another. Every community has its own accepted-provider list, so the same guarantor may be accepted at one property and rejected at another. Our list to you matches both sides.

Here’s how the three most widely accepted providers compare:

| Provider | Typical Fee (of annual rent) | Income Underwriting |

|---|---|---|

| Insurent | 6%-13% | Around 27.5x monthly rent |

| TheGuarantors | 5%-10% | More flexible; credit + employment |

| Jetty | 5%-10% | Common at larger PMC portfolios |

Total move-in cost math

Before you pay a guarantor fee, run the full move-in math. A representative example on $1,500 monthly rent:

- First month’s rent: $1,500

- Security deposit (usually one month): $1,500

- Risk fee (if a broken-lease community also charges one): $500

- Guarantor fee (8% of annual rent): $1,440

Total move-in: ~$4,940. It’s a lot. If a community you can access without a guarantor is available in your target city, you often save two grand by taking that route. If it’s the only way into a community that fits your job, budget, and location, the fee unlocks something the fee saves you elsewhere. We do this math with you before you commit.

The “will they accept it” question

We never send a client to a community with a guarantor without confirming first that the community accepts that specific provider for a broken-lease application. Getting denied after paying a $1,500 guarantor fee is the worst outcome we can prevent — and it’s entirely preventable if you check before you commit. It’s part of how we find apartments that accept broken leases that will actually honor a guarantor for your scenario.