How a Third-Party Guarantor Works for a Broken Lease

A third-party guarantor co-signs your lease for a fee, covering financial risk. How it works, what it costs, and how landlords view it.

From our daily experience reviewing applications, a past rental mistake often feels like an automatic denial.

Property managers naturally view these records as serious liabilities. We constantly see applicants confused about their options.

You might ask, how does a guarantor work for apartment approvals when a past broken lease is involved?

This guide explains the exact mechanics of third-party guarantors, the 2026 fee expectations, and why community acceptance varies so wildly.

What a guarantor actually is

A third-party guarantor is a corporate entity that co-signs your lease and assumes financial liability if you default on rent payments. This structure is completely different from using a family member as a personal co-signer.

Personal co-signers typically need a U.S. credit score over 700 and an income of 80 times the monthly rent to qualify. We recommend institutional guarantors precisely because most renters do not have personal contacts who meet those extreme financial hurdles.

Several major providers dominate the U.S. market in 2026:

- Insurent: Accepted in over 775,000 apartment units nationwide.

- TheGuarantors: Protects over $7 billion in total lease value.

- PandaGuarantee: Known for accepting lower U.S. credit scores around 500.

From the community’s side, this third party guarantor apartment service acts as an ironclad financial backstop. From your side, paying their service fee grants you access to properties that would normally reject a broken lease instantly.

The fee model

Guarantor fees are strictly non-refundable premiums paid upfront to cover the company’s underwriting and risk during your lease. These companies base their pricing entirely on your specific risk profile, including credit history and income stability.

We actively track these costs to ensure our clients budget correctly. In 2026, a standard institutional guarantor charges a one-time fee between 50% and 110% of one month’s rent.

If you are applying for a $2,000 per month apartment, this percentage translates to a significant upfront cost.

| Applicant Profile | Typical Fee Range | Estimated Cost ($2,000/mo Lease) |

|---|---|---|

| Strong Credit & Steady Income | 40% - 60% of one month’s rent | $800 - $1,200 |

| Moderate Credit & Income | 65% - 85% of one month’s rent | $1,300 - $1,700 |

| Broken Lease or Low Credit | 90% - 110%+ of one month’s rent | $1,800 - $2,200+ |

Most providers land in the 6% to 8% of annual rent range for standard applications. The fee acts similarly to an insurance policy, meaning you do not get this money back at move-out.

While most companies require the full amount at lease signing, newer platforms like Leap occasionally structure the cost as a smaller upfront payment mixed with a monthly premium. Always read the exact terms before committing to a provider.

What the guarantor covers

If you default on your rent, the guarantor immediately pays the apartment community the owed balance. The community’s financial risk is completely neutralized by this corporate backing.

This setup ensures the landlord avoids lost income and costly eviction proceedings. We view this as a highly effective tool for securing housing, but applicants must understand the financial reality.

The corporate safety net does not extinguish your personal obligation to pay for the housing. You still owe the exact same amount of money, but your debt simply transfers to the guarantor company.

“A corporate guarantor protects the property owner, not the tenant. If you default, the guarantor will pursue you for the full balance.”

The guarantor’s collection process is often aggressive and fast. They will report the unpaid debt to major credit bureaus, dispatch third-party collection agencies, and potentially file a lawsuit for the balance. Having a lease guarantor explained properly means understanding that it shifts the immediate risk away from the landlord while keeping you fully accountable.

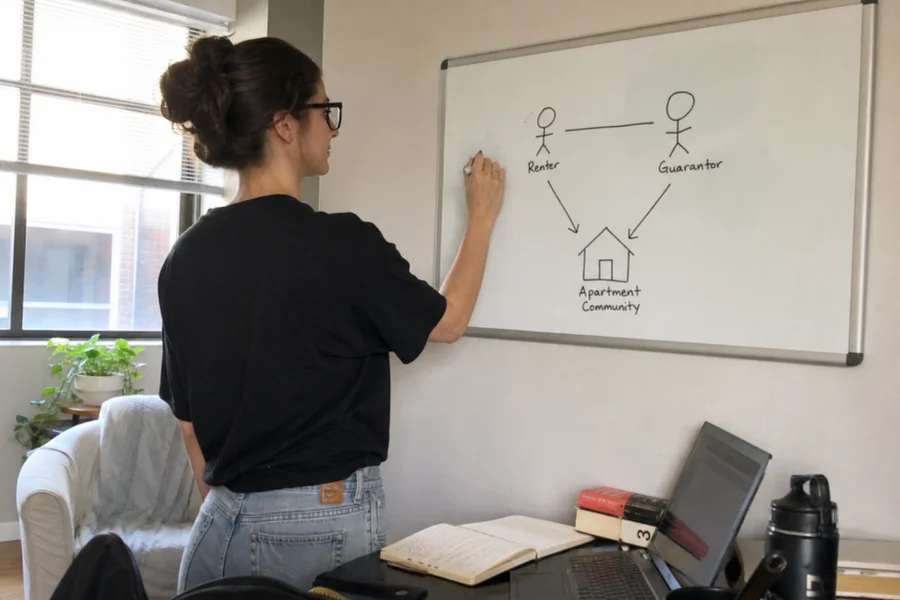

Why some communities accept guarantors for broken leases and some don’t

Corporate guarantors solve the financial risk of unpaid rent, but they cannot fix behavioral risk. A property manager looking at a broken lease sees two distinct threats: the loss of money and the hassle of a problematic tenant.

We classify apartment communities into two distinct categories based on how they view these risks.

Financial-Risk-Oriented Communities

These properties care primarily about guaranteed revenue. They are typically newer, highly competitive developments leaning into flexible criteria to attract applicants and fill empty units. Because a corporate backer ensures the rent gets paid, these managers gladly accept guarantors for broken-lease scenarios.

Behavioral-Risk-Oriented Communities

These properties prioritize tenant stability and quiet enjoyment for all residents. They view a past broken lease as a strong indicator of future behavioral issues, such as property abandonment or neighbor disputes. A corporate guarantor only solves the money problem, so these conservative communities frequently deny applications regardless of financial backing.

There is an important nuance to how case-by-case properties evaluate this behavioral risk. A broken lease caused by fleeing domestic violence, especially when documented with a protective order, is treated much differently than a simple refusal to pay rent.

Because management criteria remain unpublished, tracking these exact property preferences is essential. Applying blindly often results in paying a non-refundable application fee only to face a harsh denial.

How the application flow works with a guarantor

Securing your apartment requires a highly coordinated approach to avoid wasting money on application fees. The standard processing timeline takes one to three business days once you engage the provider.

We tell every applicant to secure their corporate backing before paying any property-level deposits.

Here is the exact step-by-step workflow for 2026:

- Apply at the community: Submit your application, knowing the broken lease will flag the system.

- Verify accepted providers: The community will require a guarantor. You must choose a specific provider they already work with, such as Insurent or Jetty.

- Apply for the guaranty: Submit your income and credit documentation. Providers like PandaGuarantee or Cosign can sometimes issue pre-approvals in just 30 minutes.

- Secure the approval letter: The guarantor evaluates your broken lease and issues formal approval to the leasing office.

- Finalize the move-in: You pay the first month’s rent, your standard deposit, and the non-refundable guarantor fee.

The guarantor’s legal obligation runs through the entirety of your lease term.

If you are ready to tackle this process, taking immediate action to verify your credit and research local property requirements is your best next step. Understanding how does a guarantor work for apartment applications is only the first piece of the puzzle, so start gathering your financial documents today.

Related reading

Frequently asked

What does a guarantor actually do?

They co-sign your lease and agree to cover rent if you default. From the community's perspective, financial risk is covered by the guarantor's underwritten income and their contractual obligation.

How much does a guarantor cost?

Typically 5-12% of annual rent, paid up-front. On $1,500 rent that's roughly $900-$1,800. The fee is non-refundable and comes on top of first month's rent and security deposit.

Do all communities accept guarantors?

No. Some communities don't work with guarantor providers at all, and some don't accept guarantors for broken-lease scenarios specifically. Verification before you commit is essential.

Turn this into a placement.

Our agents will match you with Texas communities that fit your specific scenario.