Should I Pay Off a Broken Lease Collection Before Applying?

Paying can help placement — or reset the reporting clock. When to pay, when to settle instead, and how move-in urgency changes the answer.

If your broken-lease debt is in collections, deciding whether to pay it off before applying is a real trade-off. The right answer depends on your target communities’ policies, the age of the debt, and how urgently you need to move. This guide walks through the framework we use with clients.

When paying helps your placement

Paying a broken-lease collection helps most when:

- You’re applying at communities that distinguish paid from unpaid collections. Some Texas communities’ policies specifically read “paid collections are considered case-by-case; unpaid collections are decline.” Paying moves you from decline pile to review pile.

- You want to eliminate a risk fee. At case-by-case communities, paid documentation often eliminates the risk fee that would otherwise be charged for the broken lease.

- The collection is recent (under 3 years) and on your credit report. A recent unpaid collection is a bigger scoring problem than a recent paid one at most credit-checking communities.

- You have time. Settlement and payment take 2-6 weeks including debt validation, negotiation, and documentation.

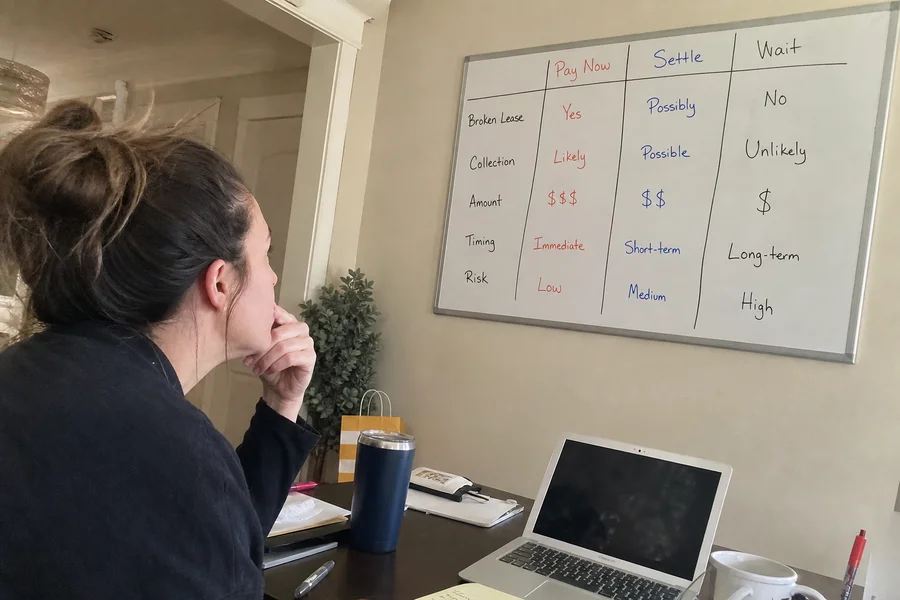

When to settle instead of paying in full

Settling makes more sense than paying in full when:

- You can’t afford the full balance. A settlement of 40-70% of the balance is often accepted by NCS or IQ Data. Half the money out, same functional resolution.

- The debt is older or past the Texas 4-year statute. Older debt settles cheaper because the agency’s leverage is lower.

- Your target communities don’t distinguish paid from settled. If the community reads “resolved” letters favorably regardless of paid vs settled, take the cheaper option.

When to wait (or apply as-is)

Waiting or applying as-is is the right move when:

- The debt is close to the Texas 4-year statute. Once past the statute, they can’t sue and settlement leverage improves. Some communities also treat statute-barred debt as functionally resolved.

- You need to move now. Settlement negotiations don’t wrap in days. If your timeline is tight, apply immediately to friendly communities and consider settling in parallel if you have time.

- Your income and offset profile is strong. If you can clear 4x rent easily and have positive rental history since, some communities approve without regard to the collection.

- You’re close to a mortgage application. Paying an old collection can temporarily hurt credit scores through re-aging. If you’re mortgage-shopping in the next 12 months, pause and consult a mortgage broker before paying.

The re-aging risk in plain terms

Some credit scoring models weight “recency of last activity” heavily. When you pay an old collection, the account gets a fresh “last activity” timestamp — the payment date. In some models, that makes the account look like a recent problem instead of an old one.

This effect is minimal for very old debt (5+ years) and usually inconsequential for rental applications specifically. But it’s a real consideration if you’re planning to apply for a mortgage soon, where scoring models are more sensitive to activity timing.

Framework

Rough decision tree:

- Balance < $500, affordable, target communities distinguish paid from unpaid: Pay in full.

- Balance $500-3,000, target communities distinguish paid from unpaid, timeline > 6 weeks: Settle for less.

- Balance any amount, past Texas 4-year statute, timeline flexible: Wait for statute leverage; consider dispute if inaccurate.

- Move-in date < 4 weeks: Apply now to friendly communities. Handle debt on parallel track if possible.

- Strong income (4x+ rent), positive history since break: Apply as-is at income-friendly communities.

Our Broken Lease in Collections service runs this decision with you based on your specific situation.

Related reading

Frequently asked

Will paying my broken lease collection guarantee approval?

No. Paying can widen your options, but it doesn't override a community's other criteria (income, timing, other rental-history issues). And at some communities, settling is smarter than paying in full.

Could paying the collection actually hurt me?

It can, with some scoring models — paying can update the 'date of last activity' and make the account look newer on your credit report. For housing this rarely matters; for a near-term mortgage application it can.

Should I pay if I need to move now?

Often applying to friendly communities first is faster than paying, because settlement negotiations take weeks. We can weigh timing with you before you commit either way.

Turn this into a placement.

Our agents will match you with Texas communities that fit your specific scenario.