Does a Broken Lease Still Show After the Lookback Window Closes?

Yes — a broken lease can still appear on screening even after the lookback window closes. Why appearance doesn't equal denial.

Our clients frequently ask: does old broken lease still show on screening after the initial penalty period ends?

That lingering mark creates confusion for property owners and anxiety for applicants. We see this issue pop up constantly in background check evaluations.

The key is separating a record that simply appears on the report from a record that triggers a hard denial.

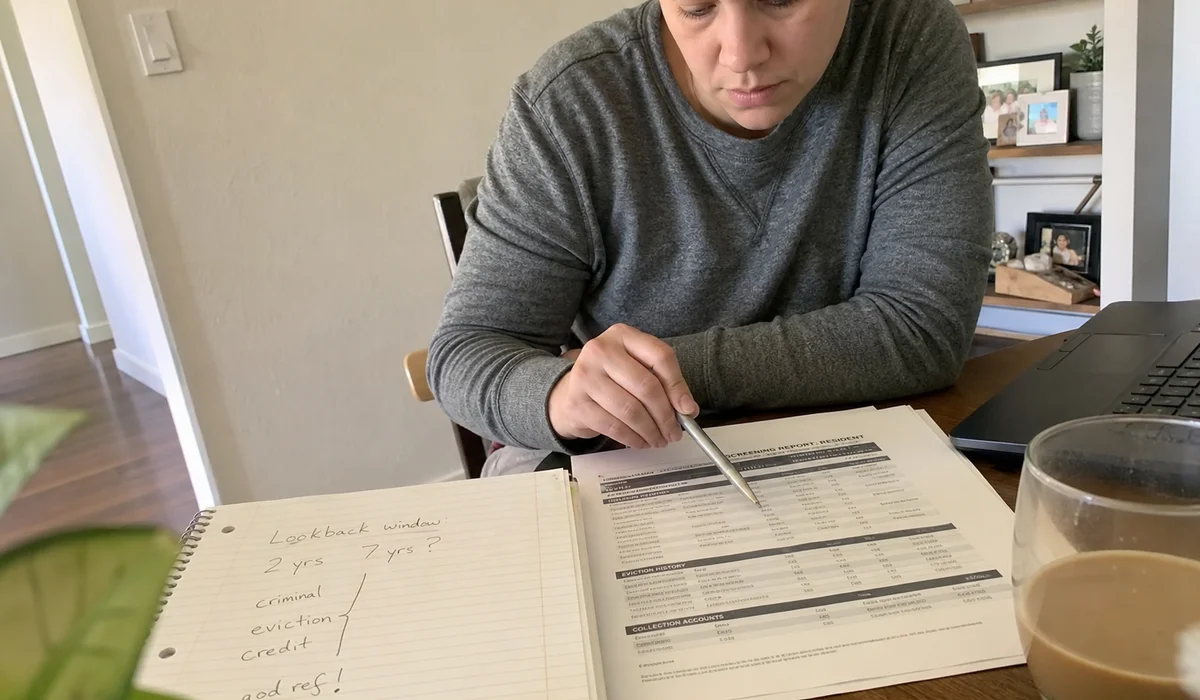

Vendor retention vs community scoring

Screening vendors maintain data for a set retention period, while individual property managers set their own lookback windows for scoring. Even after four or five years, a broken lease still shows up on a standard background check. We want to clarify exactly why this happens.

Under the Fair Credit Reporting Act (FCRA), credit bureaus and tenant screening agencies can legally report negative information like collection accounts and broken leases for up to seven years. Major industry vendors follow these federal guidelines strictly. CoreLogic SafeRent and RealPage LeasingDesk configure their databases to retain this historical data for the full seven-year allowable period.

Our experience shows that the vendor merely supplies the data, rather than making the final housing decision. You establish the rules for your specific property by setting a lookback window. Many modern apartment communities configure their screening software to only score lease breaks that occurred within the past 36 months.

| Concept | Who Controls It | Typical Timeline | Impact on Applicant |

|---|---|---|---|

| Vendor Retention | Screening Agency (e.g., CoreLogic) | Up to 7 years (FCRA limit) | Record populates on the report. |

| Community Scoring | Property Manager | 24 to 36 months | Record triggers an approval or denial. |

If an applicant has a four-year-old broken lease, the software will surface the record without penalizing their current community score. This mechanism means the exact same historical data point leads to completely different outcomes depending on your custom property criteria.

Why this makes renters anxious

Renters often panic when they see an old broken lease on report documents, mostly because the raw data displays the debt plainly without indicating how it impacts your final decision. The applicant sees the exact name of their previous property, the old move-out date, and the specific balance owed. We know this level of visibility causes immediate stress.

The 2025 Zillow Consumer Housing Trends Report reveals that the median age of a renter has climbed to 42 years old. Many of these older applicants carry extensive rental histories containing a mix of positive and negative marks. Our property management partners report that applicants frequently assume any visible negative mark means an automatic rejection.

Pro Tip: Tell an applicant your specific lookback window before they apply. This stops qualified candidates from withdrawing their applications out of fear.

A simple conversation early in the process changes everything. You can explain that an isolated incident falls outside your active criteria. The software evaluates the old record and simply flags it as a non-trigger event.

Removing an old record

Neither an applicant nor a property manager can delete a factually accurate broken lease simply because time has passed. The record remains intact for the vendor’s standard retention period unless there is a verifiable error. We always advise clients to understand the legal boundaries of data removal.

Under FCRA Section 611, an applicant possesses the right to dispute inaccurate information directly with the screening agency. Experian RentBureau and TransUnion SmartMove must investigate these consumer disputes within a strict 30-day timeline. If the agency cannot verify the details within that window, they must remove or correct the item.

Our team frequently sees these specific, dispute-worthy inaccuracies pop up in our daily reviews. You should instruct applicants to look out for the following issues:

- Inflated balances. A previous landlord may have added unjustified charges to the ledger after the tenant moved out.

- Incorrect community names. Automated matching algorithms sometimes assign a duplicate entry or link a file to the wrong property.

- Inaccurate dates. A wrong move-out date could artificially pull an older record into your current 36-month lookback window.

Correcting even a minor error can shift the outcome of an application significantly. An applicant disputing a $3,500 balance down to a verified $1,200 might suddenly pass your software’s specific debt-to-income threshold.

What communities actually weigh outside the window

Leasing agents note the historical event without letting it trigger an automatic denial if the record falls outside the active window. You instead shift your focus to the applicant’s current financial reality and recent behavior. We recommend adopting a comprehensive approach for these older cases.

Property managers typically prioritize recent performance metrics to gauge risk accurately. A 2025 Zillow report highlighted that 95% of modern renters consider staying within their budget essential. This laser focus on affordability often translates into better payment reliability today, regardless of a mistake made five years ago.

Our top property owners evaluate these specific current factors when reviewing a file. You should look for these positive indicators before making a decision:

- Recent rental history. Agents look for clean tenancy records over the immediate past 24 to 36 months.

- Income and employment stability. The industry standard requires a gross monthly income equal to three times the rent.

- Current credit report health. Evaluators review active tradelines and check if the old property debt remains an open collection account.

- The broader behavioral trend. A single broken lease from 2021 matters far less than three late payments in 2025.

The older lease break functions as just one minor data point rather than a hard roadblock. You can confidently approve the application if the candidate demonstrates strong recent financials. When a client asks, “does old broken lease still show on screening checks,” you can explain that while the answer is yes, that visibility does not equal an automatic denial. We encourage you to review your property’s custom lookback window settings today to ensure you are not turning away great applicants.

Related reading

Frequently asked

If it still shows on my report, will I be denied?

Not usually. Once outside a community's lookback window, the record appears but rarely triggers denial. Some conservative communities still weigh older events; most don't.

Can I get an old broken lease removed from my report?

Only if it's inaccurate. If the record is factually correct, it stays for the vendor's retention period (typically up to 7 years). You can dispute inaccuracies under the FCRA.

How long until it's gone from my record entirely?

Rental-history vendors typically retain records for up to 7 years. Even after it stops mattering to communities (2-3 years past the event at most), the record may remain visible for several more years.

Turn this into a placement.

Our agents will match you with Texas communities that fit your specific scenario.