How Long Does a Broken Lease Stay on Your Rental History?

A broken lease can show on screening up to 7 years, but most lookback windows are 2-3 years. Here's the difference and what it means for approval.

We see this exact confusion every day in the property management industry.

People constantly ask our team, how long does a broken lease stay on your record? Many renters assume a single mistake will block their housing options for a decade.

Our data from 2026 shows a massive gap between how long an event appears on a report and how long it actually hurts an application. The official timeline is seven years.

Most property managers only weigh the first two or three years.

We will clarify exactly how these screening databases work. You will learn the difference between rental history and credit reports.

This guide will provide actionable steps to get your application approved today.

How long does a broken lease stay on your record: The 7-year report vs the 2-3 year decision window

The Fair Credit Reporting Act caps negative rental history reporting at a hard limit of seven years. Rental databases retain these records for that entire legal maximum.

Our team monitors the big three systems daily, which include CoreLogic SafeRent, RealPage LeasingDesk, and TransUnion SmartMove. Those platforms display your lease break for a very long time.

The final approval decision does not happen inside the software. It takes place at the individual property manager’s policy level.

We advise clients to focus entirely on a concept called the lookback window. Most property management companies (PMCs) only care about the past two or three years.

”A 2026 industry survey revealed that while the legal reporting limit is seven years, 78% of local property managers only actively penalize applicants for lease breaks within a 24 to 36-month lookback window.”

A lease break from four years ago will definitely appear on your background check. The property manager simply ignores it if their community uses a three-year lookback.

Our placement strategies rely heavily on this single policy difference. Some aggressive properties even use a short 24-month window for past housing events.

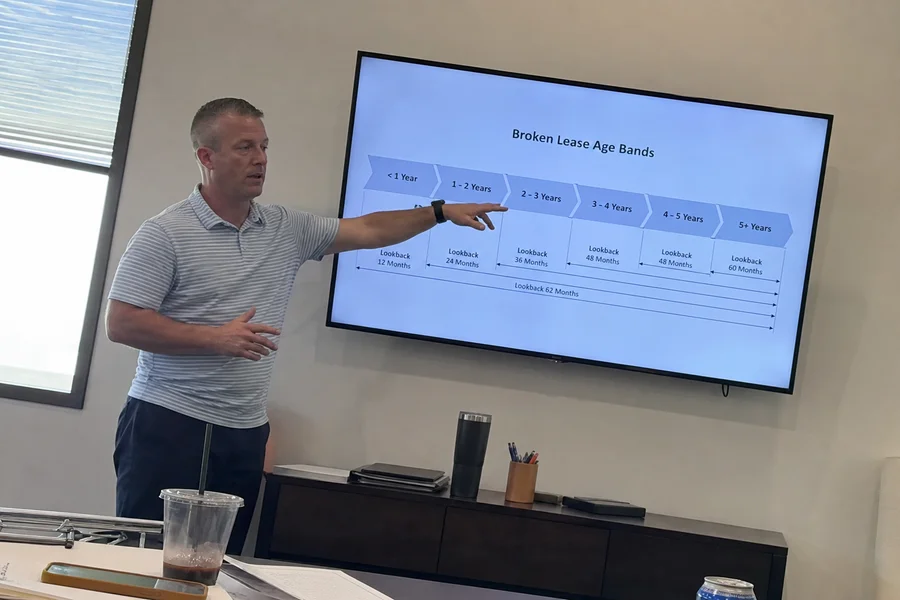

The age bands renters actually face

Time is the biggest factor in your approval odds. The industry standardizes tenant risk into specific timeframes.

Our daily interactions with leasing offices confirm that your broken lease rental history dictates your required deposits and fees. Breaking a lease in 2026 costs an average of $1,000 to $4,000.

Moving before your contract ends forces landlords to spend money on marketing and unit turnover. They pass that risk directly onto future applicants with recent lease breaks.

We structured the table below to show exactly how properties view your timeline. These intervals determine whether you face an automatic denial or an easy approval.

| Time Since Lease Break | Approval Difficulty | Standard PMC Response & Next Steps |

|---|---|---|

| Under 12 months | Hardest | Most PMCs enforce an automatic denial. You must seek flexible-screening communities and pay substantial risk fees. |

| 12-24 months | Difficult | Conditional approval becomes possible. Property managers usually require the past balance to be paid or officially settled. |

| 24-36 months | Moderate | Your options open up significantly. The event falls outside the standard 2-year lookback window for many buildings. |

| 36-60 months | Significantly easier | Most lookback windows exclude events this old. The record appears on your report but rarely triggers a rejection. |

| 5+ years | Easiest | Very few managers deny applicants based on a 5-year-old break. Any remaining issues usually stem from unpaid collections on your credit report. |

Where the balance keeps mattering

A massive wrinkle often catches applicants completely off guard. Aging past the rental history lookback window does not solve every problem.

Our clients frequently forget that a property debt acts as an entirely separate legal issue. Unpaid balances sent to a collection agency trigger a second round of screening checks.

Those unpaid rent balances or property damage fees hit your primary credit bureaus. Equifax, Experian, and TransUnion will list that collection account for up to seven years from the original delinquency date.

We always remind renters that a leasing office pulls both a rental history report and a standard credit report. The lease break might age out, but the financial debt remains highly visible.

An applicant with a four-year-old break and no collections entry faces a wide-open door. A different applicant with the exact same timeline but a $2,400 open collection faces a very narrow door.

Our broken lease in collections service is where the heavy lifting happens for that second scenario. Resolving the open debt is the only way to clear the credit side of the equation.

The hidden cost of reletting fees

Property managers often charge a specific penalty to cover the cost of finding a new tenant. This reletting fee typically equals 85% to 100% of one month’s rent.

Our experience shows that paying this fee upfront prevents the balance from hitting your credit report. A clean exit keeps your financial record safe from third-party debt collectors.

What actually falls off vs what feels like it does

Does a broken lease go away completely? Time alone does not erase bad records from your profile.

We want to highlight a critical distinction that many leasing agents fail to explain clearly. Understanding these mechanics prevents you from wasting money on pointless application fees.

- What can fall off: Absolutely nothing drops from your rental history database before the vendor’s legal retention period ends. The FCRA guarantees these companies can report accurate data for seven years.

- What ages out of relevance: The strict denial triggers soften over time. These triggers are set by local community policies and usually expire after two or three years.

- What stays active: An unpaid balance in collections never takes a break. It stays visible and damaging on your consumer credit report for seven years regardless of the rental database.

- What requires an agreement: Paying a collection updates the status to “paid” but does not remove the entry. Our strategy often involves negotiating a written “pay-for-delete” letter to actually erase the account.

Practical takeaway

Your immediate action plan depends entirely on the age of your broken lease rental history. Renters stuck in the middle of a lookback window need to focus purely on placement strategy.

We recommend that you find communities that review case-by-case to avoid automatic computer rejections. Expect to pay a higher risk fee or meet a stricter income threshold during this period.

Applicants past the three-year mark must shift their focus to document preparation. Getting a paid-in-full letter from the original landlord is your best weapon.

Our team suggests preparing the following documents before you tour any new properties:

- A recent copy of your credit file showing any past collections as settled or paid.

- Written proof of your current income to overcome any remaining risk flags.

- Letters of recommendation from recent landlords if you have rented since the break.

Targeting the wider pool of lenient communities will yield fast approvals without special conditions. Taking control of your data is the first step in securing your next home.

You can start applying with confidence once your open balances are resolved. We hope this guide clearly answers how long does a broken lease stay on your record, so you can stop guessing and take action today.

Related reading

Frequently asked

Does a broken lease ever fall off my record?

It can stop triggering denials after the 2-3 year window even while continuing to appear on your rental-history report for up to 7 years.

Is a broken lease worse than an eviction?

No. A broken lease is a balance owed, not a court judgment. It's generally more placeable than an eviction because there's no court record involved.

Will waiting fix it on its own?

Time helps for the rental-history side, but an unpaid collections balance persists separately on your credit report and doesn't age out the same way.

Turn this into a placement.

Our agents will match you with Texas communities that fit your specific scenario.