Can I Rent If My Broken Lease Was More Than 3 Years Ago?

A broken lease over 3 years old usually falls outside most lookback windows, so it rarely triggers denial. What still matters at this age.

As a business owner or a homeowner stepping back into the rental market, you might worry that an old leasing mistake will ruin your chances.

We see professionals panic over past financial decisions constantly. That 36-month mark is actually the critical dividing line for your approval.

If you had a broken lease more than 3 years ago, your placement outlook is significantly better than a recent-break renter. Most Texas communities will not trigger an automatic denial on a break this old.

Our property specialists know that the record simply ages past their lookback window and stops being a scoring factor. This guide breaks down exactly how property algorithms view older records in 2026, and outlines the actionable steps you should take next.

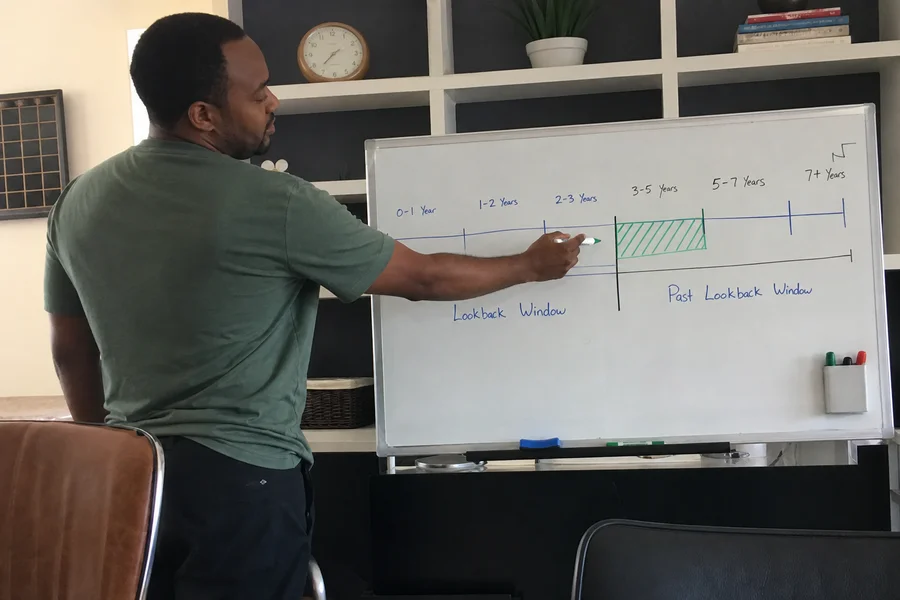

Why 3+ years usually clears the window

Most property management companies set their automated screening software to a strict 24 or 36-month lookback period. A broken lease from over three years ago simply falls outside this active scoring zone.

We see this software automation save applicants time and stress. Most Texas communities use a 2 or 3-year lookback window for their standard approvals. A broken lease from 36 months ago clears a 24-month window and sits at the edge of a 36-month window.

From 40 months on, you are completely clear at both of those common thresholds.

Our data shows that from 48 months on, you are outside virtually all commonly used lookback windows. That does not mean every single community will approve you. Some conservative property management companies use 4 or 5-year windows.

Our team tracks the exact algorithms used by major screening platforms like RealPage and Yardi. These platforms allow landlords to configure their own rules, but the industry standard defaults to a maximum 36-month history check.

Those conservative outliers are the minority, but they definitely exist in the 2026 market. Even at stricter properties, a 5-year-old break with paid documentation is typically approvable. You just face slightly more scrutiny than at a standard 2-year-window community.

Our property specialists categorize these lookback windows into three common tiers:

- Class A Luxury Apartments: Often use a strict 36 to 48-month window.

- Class B Suburban Properties: Typically stick to the standard 24 or 36-month limit.

- Class C Value Communities: Frequently ignore anything older than 12 to 24 months.

What can still trip you up

Three specific factors can still cause friction at 3 to 5 years: unresolved collections, multiple rental history events, and conservative company policies. You must address these items to secure an approval.

We always warn clients that a clean rental database search does not guarantee a clean credit report. The following roadblocks frequently catch renters off guard:

- Collections on credit report: If the debt went to collections, that account stays on your credit report for exactly 7 years from the original delinquency. This time limit is strictly enforced under the federal Fair Credit Reporting Act (FCRA). Experian is particularly fast at flagging these old collection accounts, which can trigger an automatic credit-side denial.

- Multiple rental-history events: If the broken lease is one of two or three concerning items on your rental history, the pattern reads differently than an isolated event. Throwing a late-fee notation or a partial eviction into the mix makes landlords nervous. Some communities use third-party databases like RentGrow to look at this historical pattern regardless of age.

- Conservative PMC policy: A small subset of communities weight any historical rental issue regardless of age. There are few of these conservative properties, but you will bump into them occasionally in the 2026 market.

Each of these roadblocks has a specific workaround. Our credit experts put together the collections guide to walk you through the exact credit-side handling process.

Pattern issues respond well to a letter of explanation and current positive references. Conservative management companies are simply avoided in your shortlist.

Documentation you still want

You still need to provide a paid-in-full letter, positive landlord references, and standard proof of income to secure your new place. Having this documentation ready smooths the process immensely, even in the 3 to 5 year band.

Our team recommends gathering these specific files before you even submit an application:

- Paid-in-full letter: Securing this document proves the balance is settled, removing doubts for the new property manager. Even if the community will not require it, providing it upfront removes any friction.

- Positive landlord reference: A quick email or letter from any lease you have completed since the incident shows you are a responsible tenant today. One or two references from later tenancies are incredibly strong.

- Standard proof of income: You need two recent pay stubs from 2026 or an official employment letter. No inflated income multiplier is needed at this age, so proving you earn 3x the monthly rent usually suffices.

Landlords want to see clear evidence that you can easily manage the monthly payments. Our financial experts note that this 3x multiplier stems from standard U.S. Department of Housing and Urban Development (HUD) affordability guidelines.

This translates to a safe 30% to 33% rent-to-income ratio.

What the application experience looks like

Your application experience will feel completely normal if you apply at a community outside your specific lookback window. You simply pay the application fee, undergo screening, and await the decision.

We see applicants get approved with standard terms every single day. There is no risk fee, no inflated deposit, and just the standard income multiplier.

At a community inside your window, you might still face a small risk fee or a higher deposit. A 2-year window community reviewing a 30-month-old break is a prime example.

Our leasing agents notice that these terms are typically much lighter than a recent-break scenario. You avoid the heavy penalties associated with fresh evictions. You can clearly see the difference in financial requirements when comparing fresh breaks to older ones.

| Application Factor | Recent Break (Under 2 Years) | Older Break (3 to 5 Years) |

|---|---|---|

| Risk Fee | $500 to $1,000 (Non-refundable) | $0 to $250 |

| Security Deposit | 2x Monthly Rent | Standard (Often $200 to 1 Month) |

| Guarantor Required | Almost Always | Rarely Needed |

This table illustrates exactly why waiting past the 36-month mark makes financial sense.

Related reading

- Older Broken Lease (2-5 Years), the placement service

- What is a lookback window and how does it work?

- Paid vs unpaid older broken lease: does it still matter?

Reviewing these resources will help you successfully secure a new place. Having a broken lease more than 3 years ago does not have to stop you from moving forward.

Our team is ready to help you complete this process. Contact our office today to start your application.

Frequently asked

Is a 3-year-old broken lease basically fine for renting?

Often yes. It usually falls outside a 2- or 3-year lookback window, so it typically won't trigger automatic denial. An unpaid balance in collections can still create a separate credit-side issue.

Does the break still show on my report?

Yes — rental-history vendor retention is usually 7 years or more, so it may still appear. But appearance doesn't equal denial once past the community's lookback window.

Do I still need documentation?

Lighter than for a recent break, but a paid-in-full letter (if applicable) or a positive rental reference since still speeds approval and can eliminate any residual fee some conservative communities might charge.

Turn this into a placement.

Our agents will match you with Texas communities that fit your specific scenario.