How Income and Employment Stability Offset a Broken Lease

When there's no history to offset a break, income does the work. How income multipliers, employment length, and proof-of-income drive approval.

We see this scenario play out daily across the leasing industry. A broken lease without recent rental history sets off immediate alarms.

Our focus must immediately shift to finding an income employment offset broken lease solution to minimize that perceived risk.

This guide breaks down the math leasing offices use today, the documentation that holds up under modern scrutiny, and the actionable workarounds to secure an approval.

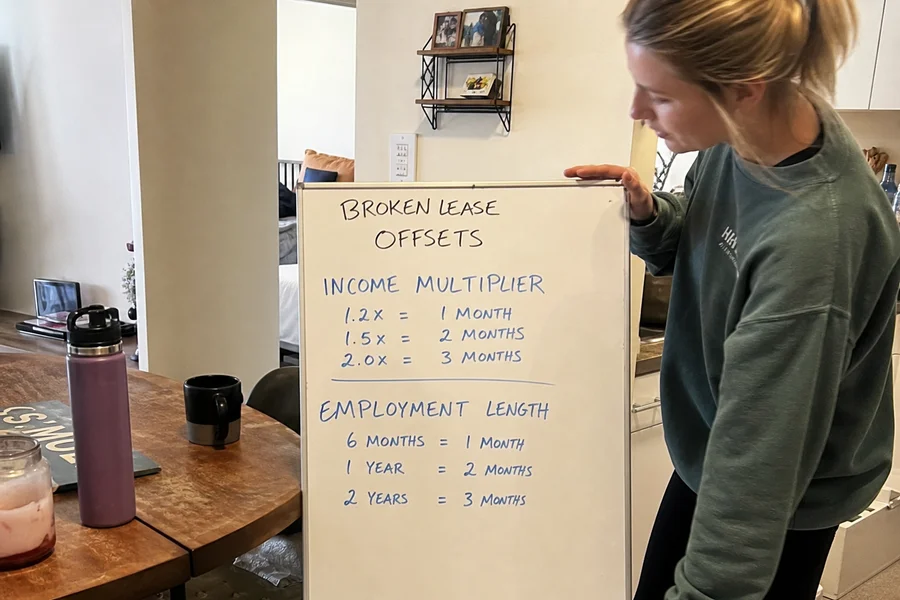

The income math

We know property management software platforms automatically flag applications that fall below specific baseline ratios. The income math revolves around a strict multiplier comparing your gross monthly income to the monthly rent.

Our team tracks these requirements closely across different property types, noting that the national average US rent sits at approximately $1,645 in 2026. Hitting just the standard 3x multiplier for an average unit requires an annual gross income of nearly $60,000, and this steep curve gets steeper if you have a compromised rental history. Let’s look at the breakdown for a typical $1,500 per month apartment.

| Multiplier Requirement | Scenario Context | Gross Monthly Target |

|---|---|---|

| 3x Rent | Standard baseline for most US and Texas applications | $4,500 |

| 3.5x Rent | Common bar for broken-lease applications | $5,250 |

| 4x Rent | Conservative communities or very recent broken leases | $6,000 |

We always advise applicants to confirm the target property’s exact multiplier before submitting non-refundable fees. Systems like Yardi or RealPage process these numbers rigidly, meaning a discrepancy of just a few dollars can trigger an automatic denial.

What counts toward income

Communities primarily count verifiable W-2 wages, 1099 earnings, and official government or retirement benefits, requiring that income be consistent, documented, and reliably deposited. We see a major shift in how this income is vetted in 2026, with landlords now utilizing specialized fraud detection platforms like Snappt.

A recent Snappt report identified a 5.1% fraud rate across millions of rental applications this year, meaning property managers scrutinize pay stubs closer than ever to spot manipulated forms. Our advice is to provide pristine documentation for the four main categories of accepted income:

- W-2 salary and hourly wages: Verified via pay stubs and an official employment letter.

- 1099 self-employment income: Verified via tax returns and a consistent deposit history.

- Benefits and support: Alimony, child support, disability, or retirement funds verified via award letters and bank deposits.

- Variable pay: Overtime, commissions, and bonuses verified via YTD pay stub inclusion if they show consistency.

Variable income policies differ widely by community, as some communities cap variable pay at a specific percentage of your base salary, while others exclude it completely. We suggest leaving expected future income off the table unless backed by an ironclad offer letter.

Property managers will not count a job offer starting next month unless the letter is fully dated and specifies the start date. One-time payments and family gifts also fail to meet the stable income criteria.

Why employment length matters

Employment length serves as an indicator of income durability, which directly reduces a landlord’s financial risk because a long tenure proves you can maintain a steady cash flow. Our perspective on employment history mirrors how a bank views a loan application, meaning if two applicants show identical monthly income, the one with a longer job tenure always wins.

The Bureau of Labor Statistics reported in 2024 that median employee tenure in the private sector hit a 20-year low of just 3.5 years. We know that presenting a 12-month tenure stands out positively against this national backdrop, so here is how leasing offices interpret your timeline:

- 12+ months at the same employer: Reads as highly stable. It signals durable, dependable income.

- 6 to 12 months: Reads as acceptable. It is not a red flag, but it lacks premier strength.

- Under 6 months: Reads as a notable risk. A new job could end quickly, making income durability uncertain.

- Multiple job changes in 2 years: Reads as chronically unstable regardless of your current paycheck.

Our strategy relies on compounding stability, as strong income paired with a stable, long-term job reads much better than identical income at a brand-new position. A solid tenure track record minimizes the perceived risk of past rental mistakes, which is why employment stability apartment approval criteria are so strict.

Documentation to bring

A standard package for a broken-lease application relying on income includes your two most recent pay stubs, an employment verification letter, and bank statements. Having these ready in advance signals seriousness and accelerates the decision process.

We see a growing reliance on automated systems for this step, with many large property management firms now using Equifax’s “The Work Number” database for instant verification. This automated check costs the property manager money, and if your data is missing or locked, the application stalls.

Bringing hard copies ensures the process keeps moving forward regardless of digital database hiccups. Our recommended physical documentation package includes the following items:

- Two most recent pay stubs: These must show year-to-date gross income and the current pay period.

- Employment verification letter: Have HR or your manager state your role, start date, current salary, and status as a permanent W-2 employee.

- Recent bank statements: Bring two to three months of records showing consistent income deposits and a reasonable daily balance.

- Self-employed 1099 proof: Provide your most recent tax return with all pages included, plus 6 to 12 months of bank statements demonstrating steady cash flow.

We encourage applicants to organize this paperwork carefully before touring a property. Presenting a complete file upfront shows respect for the leasing agent’s time and drastically improves your chances of a manual override approval.

When income isn’t enough

Falling short of a strict 3.5x multiplier does not mean automatic rejection if you leverage alternative financial backing, such as adding a guarantor or offering a higher deposit. Our experience shows that flexibility exists if you know exactly what options to offer.

If your income clears the standard 3x hurdle but misses the broken-lease penalty threshold, third-party corporate guarantors like TheGuarantors or Rhino have become popular in 2026. These platforms act as institutional co-signers for a non-refundable fee, effectively bypassing the community’s strict income requirement, though we also see success with the following traditional strategies:

- Co-applicant: Adding a roommate or partner with strong income and a clean rental history combines your earning power.

- Personal Guarantor: A financially secure family member can underwrite the lease using their own income.

- Higher deposit: Some communities will accept an additional month of rent upfront to substitute for the income shortfall.

- Lower-rent unit: Downsizing to a $1,300 unit at a similarly good community is often smarter than stretching for a $1,500 apartment.

Detailed walk-through: First apartment after a broken lease: guarantor vs higher deposit.

Approaching the leasing manager directly with these solutions is a smart move, and our final piece of advice is to present this backup plan before they have a chance to issue a denial. This proactive approach demonstrates true financial responsibility, as you must leverage strong income to offset broken lease penalties whenever possible.

Related reading

- Broken Lease With No Rental History Since (placement service)

- Income requirements for recent broken-lease approval

- How to document private landlord or roommate rent payments

Taking action on these steps is your clearest path forward to an approval.

We recommend gathering your documents today to build a successful income employment offset broken lease strategy.

Frequently asked

How much income offsets a broken lease?

Higher multipliers (3.5x-4x rent) plus steady employment carry the most weight. Some communities focus on the multiplier; some focus on employment length; strong applications hit both.

Does job length matter?

Yes. Longer, stable employment reassures communities that income is durable. 12+ months at the same employer is a common signal of stability.

What proof do I need?

Two recent pay stubs, an offer or employment verification letter, and 2-3 months of bank statements. For 1099 or self-employed income, tax returns and consistent deposit history.

Turn this into a placement.

Our agents will match you with Texas communities that fit your specific scenario.