How to Get a Paid-in-Full or Zero-Balance Letter

A paid-in-full or zero-balance letter proves your broken lease is resolved. Who to contact, what to request, and how to use it in an application.

We regularly see mortgage applications and commercial approvals stall due to an old unresolved broken lease. Knowing how to get paid in full letter from old apartment collections is essential for clearing these background checks. A zero balance letter apartment document proves to a lender that past residential debt is completely resolved.

Our team will walk through who to contact, exactly what to ask for, and what to do if the agency stalls. This guide covers the entire process from start to finish.

You will learn the exact steps required to protect your credit profile.

Who issues the letter

We always note that the right issuer depends entirely on who currently holds the broken lease debt. You must contact the specific property management company or collection agency that owns the account right now. Many applicants waste weeks contacting the wrong corporate office.

Our advisors tell clients to start by checking their most recent U.S. credit report or collection notice. These official documents will show exactly where the debt sits today. The account is usually handled by one of three entities.

- Former community, debt not sold or referred: The community’s accounting manager issues the letter. If the same property management company still owns the building, they usually have records going back years.

- Debt sold to a collection agency: The agency now owns the debt and issues the paperwork. Common U.S. rental debt buyers include National Credit Systems, Fair Collections and Outsourcing (FCO), and IQ Data International.

- Debt referred but not sold: Either party can technically provide the document. Property managers will usually defer to the agency collecting on their behalf.

We recommend starting with the former community if you are unsure about the debt ownership. They can quickly look up your file and tell you exactly where the balance went. This simple phone call saves a massive amount of time.

What to request

Our standard protocol requires sending requests for paid in full letter rental documentation in writing via email. A written request creates a paper trail if you need to dispute the account later under the Fair Credit Reporting Act (FCRA). Collection agencies are famous for making verbal promises over the phone that they never actually fulfill.

We require clients to include several specific data points so the clerk can process the request accurately. Missing details will give the agency an easy excuse to ignore your message entirely. Your correspondence should always contain these key elements:

- Your full legal name and any name used on the original lease contract.

- The former apartment community’s name and exact U.S. address.

- Your unit number and approximate move-in and move-out dates.

- The original balance amount and the final amount paid to resolve it.

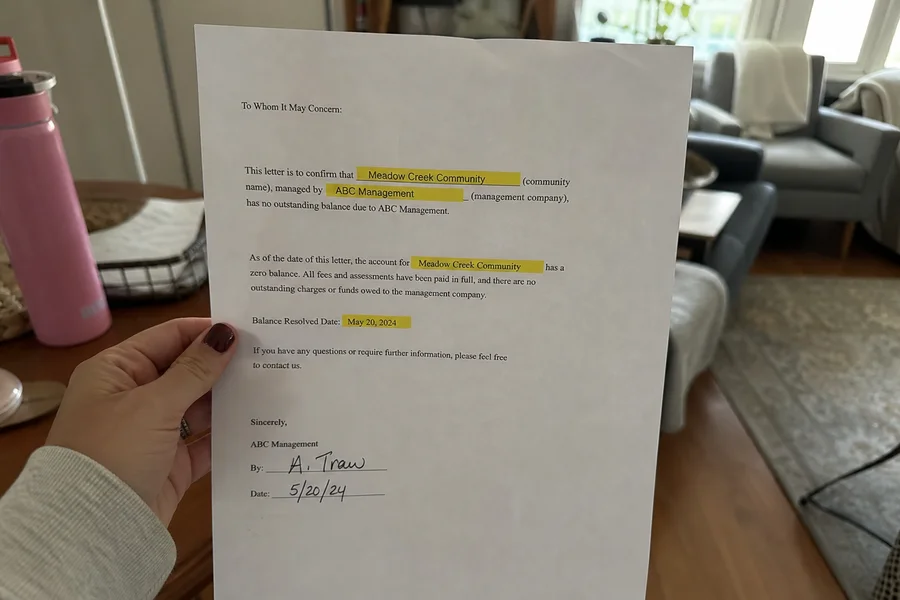

- A specific demand for a letter stating the account has a “zero balance.”

We find that a clear and concise message always gets the best response rate. Do not include unnecessary backstory or emotional complaints about the past lease dispute. A simple, professional tone is all that is required.

Our standard template is very straightforward and easy to adapt. Sample opening: “I am writing to request a zero balance letter confirming that my account at [Community Name] is resolved. I paid the outstanding balance of $X on [date], and I need this for a current commercial lease application.” This format provides exactly what the accounting department needs to pull your specific file.

Typical timelines and what to expect

We see most property communities and U.S. collection agencies respond within three to ten business days. If you have not heard anything after a full week, you must send a follow-up message. A gentle nudge usually surfaces the letter within 24 hours.

| Issuer Type | Expected Response Time | Required Follow-Up |

|---|---|---|

| Property Management | 3-5 business days | After 1 week |

| Collection Agency | 7-10 business days | After 2 weeks |

| Credit Bureau Dispute | Up to 30 days | Automatic update |

Our team suggests sending a polite second email simply referencing your original request date. The average cost to break a lease in the U.S. runs between $1,000 and $4,000 according to 2026 Zillow rental data. Resolving a balance of that size requires proper documentation to protect your credit profile.

We advise clients to negotiate the letter upfront if they are paying the debt right now. Make the physical document a non-negotiable part of your final payment terms. Saying, “I will pay the full $2,000 balance today if you provide a paid-in-full letter within two business days,” is highly effective.

Our experts warn applicants to carefully review any settlement agreement before signing or paying. Some basic settlement letters hide fine print that preserves the agency’s right to report the debt. Only accept a document that explicitly promises the account is closed with a zero balance.

What to do if they won’t provide one

We know some property managers are unresponsive, and many collection agencies deliberately stall. You need solid backup documentation if the original issuer ignores your repeated requests. Alternative proof will often satisfy a cautious underwriter or leasing agent.

Our team uses four primary alternatives when a company refuses to cooperate. You must keep a detailed record of every ignored email and unreturned phone call. Building a timeline of their negligence strengthens your case.

Bank records

We regularly use a clear screenshot or PDF of the outbound bank payment as strong proof. The bank statement must show the exact amount, the clearing date, and the recipient’s name. Lenders simply need verifiable evidence that the funds actually left your account.

Cancelled check images

Our advisors always request both the front and back images of the cleared check from the bank. Your bank’s cancelled check archive provides undeniable proof of a completed transaction. The image shows exactly who endorsed and deposited the check you sent.

Settlement agreement

We see many property managers accept a written settlement agreement alongside a matching bank receipt. The contract terms show exactly what was agreed upon to close the account. Just ensure the agreement explicitly lists the exact dollar amount required for settlement.

Third-party escalation

Our team initiates a formal credit bureau dispute immediately if an agency like Procollect ignores our calls for two weeks. Under the FCRA, credit bureaus have exactly 30 days to investigate your formal dispute. The credit bureaus will remove the collection entirely if the agency fails to respond to the investigation.

Using the letter in an application

We instruct applicants to attach the zero balance document directly to their new application along with other income proofs. You want to make it incredibly easy for the leasing agent or underwriter to see your resolution status. Reference the letter directly in your formal explanation of past credit issues.

Our favorite phrasing is very direct: “The broken lease from 2024 was resolved on [date], and a copy of the paid-in-full letter is attached.” This proactive approach stops the underwriter from hunting for answers. A clear paper trail removes the doubt that causes most application denials.

We encourage you to gather these documents today so your next application moves forward smoothly. Take action now to secure your approval. The right paperwork opens doors.

Related reading

Frequently asked

Who issues the letter?

The former community that held the original debt, or the collection agency if the debt was sold or referred to collections.

How long does it take to get?

Usually a few days to a couple of weeks after your written request. Request it in writing and follow up if you don't hear back within a week.

What if the community or agency refuses to provide one?

Bank records, cancelled check images, or a signed settlement agreement can serve as backup documentation. Some property managers will accept those in lieu of a formal letter.

Turn this into a placement.

Our agents will match you with Texas communities that fit your specific scenario.